From the editor’s

desk…

Welcome

to Pipes & Wires #104. This issue has a fairly broad topical and

geographical coverage, starting with some regulatory decisions in New Zealand and

Australia.

We

then look closely at the sale of electricity transmission grids in Germany and

summarise the deals so far, and then conclude with a mix of articles on the

European gas market, privatisation in the Philippines and electric car

recharging in the US.

Accredited supplier status

Utility

Consultants is pleased to announce that it is now an Asia-Pacific Utilities Group (APUG) accredited

supplier (registration number 88899493).

Get Pipes & Wires “white-listed”

To

avoid being intercepted by your server as spam, please arrange to have phil.caffyn@utilityconsultants.co.nz

“white-listed” by your IT people.

Pipes & Wires on the web

Pipes & Wires on Linked In

Pipes

& Wires now has an on-line

group for readers to keep in touch on a more regular basis, bounce ideas

around or raise issues and concerns. Pick here

to visit my Linked In profile and add me

to your connections.

Pipes & Wires on Facebook

Pipes

& Wires now also has its own Facebook

page. Just go to Facebook’s home page and search for Pipes & Wires.

Pipes & Wires on YouTube

To

see a short video clip explaining more about Pipes & Wires, pick here.

Pipes & Wires on the web

To

read more about Pipes & Wires, pick here.

About Utility Consultants

Utility

Consultants Ltd is a management consultancy specialising in pretty much all aspects of energy and infrastructure

networks – pick here

to see more, or to be sent a detailed profile of recent projects, pick

here.

Matters

for attention

NZ

– public safety management systems

Just a reminder that the requirement for

all electricity businesses (of more than 10MW capacity) to have their PSMS in

place and externally audited is only 7 months away. For help with compiling

your PSMS, or to have a pre-audit review undertaken, phone Phil on (07)

854-6541 or pick

here.

Regulatory

decisions

NZ – resetting the electricity default

price path

Introduction

In mid-July 2011 the Commerce Commission released its draft decision on resetting the default price paths (DPP) that it intended to apply to non-exempt electricity distribution

businesses (EDB’s) on 1st April 2012 for the remaining 3 years of

the 2010 – 2015 DPP ie. the years ending 31st March 2013, 2014 and

2015. This article examines the background and comments on some salient

features of the draft decision.

Provision for resetting mid-period

The broad legal framework for the

regulatory regime is Part 4 of the Commerce Act 1986. The Commission was required by s52P of the Act to issue a

determination setting out the requirements of the price-quality path that would

apply to non-exempt EDB’s over the period 1st April 2010 to 31st

March 2015 (the “2010 – 15 DPP”), which it did in November 2009.

Because the Input Methodologies were

still being compiled in November 2009, the Commission was able to invoke

s54K(3) of the Act which provides for the 2010 – 15 DPP to be reset if the

final Input Methodology would’ve resulted in a materially different DPP. The

Commission has argued that it would’ve, hence it is justified in resetting the

2010 – 15 DPP.

Application of claw-back

Claw-back is the process by which any

under-recovery or over-recovery in a previous period can be compensated for by

adjusting prices in a current period, and its application is set out in s52D of

the Act. The Commission does not propose to apply claw-back for this reset.

Individual company resets

The resets that the Commission intends

to apply to each EDB are as follows (MAR3 is the maximum allowable

revenue in Year 3, P3 is the reset at the start of Year 3, and X4,5

is the rate of change that will apply for Years 4 and 5. Note that a negative P3

represents a decrease, whilst a negative X4,5 represents an increase

due to the subtraction of a negative in the CPI-X component)...

|

EDB |

MAR3 |

P3 |

X4,5 |

|

EDB |

MAR3 |

P3 |

X 4,5 |

|

$30.2m |

15% |

-5% |

|

$28.4m |

8% |

0% |

||

|

$57.7m |

4% |

0% |

|

$22.5m |

8% |

0% |

||

|

$7.9m |

13% |

-10% |

|

$220.9m |

-9% |

0% |

||

|

$20.5m |

-2% |

0% |

|

$29.9m |

14% |

-5% |

||

|

$29.0m |

10% |

0% |

|

$29.6m |

20% |

-10% |

||

|

$12.8m |

3% |

0% |

|

$90.7m |

7% |

0% |

||

|

$19.5m |

-10% |

0% |

|

$399.4m |

-9% |

0% |

||

|

$6.7m |

3% |

0% |

|

$109.1m |

-4% |

0% |

Next steps

The Commission will receive submissions

on the draft decision until 11am, Wednesday 24th August, and will

receive cross-submissions until 11am, Monday 5th September.

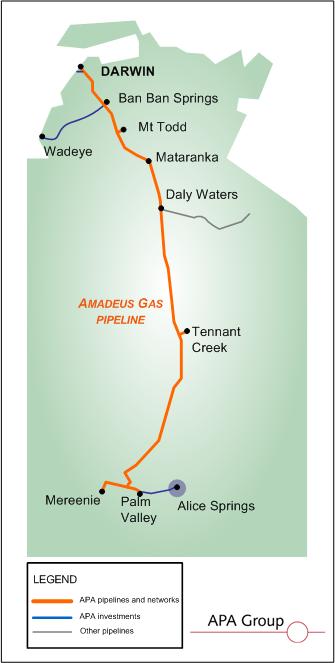

Aus – final decision for the Amadeus Gas Pipeline

Introduction

Pipes

& Wires #101 and #102

discussed NT Gas’ proposed access

arrangement for the Amadeus

Gas Pipeline (AGP) for the regulatory period from 1st July 2011

to 30th June 2016. This short article concludes that series by examining

the Australian Energy Regulator’s (AER)

final decision.

The

revised access arrangement

The following table compares the AER’s

draft decision with NT Gas’ proposed access arrangement (and will be completed

as the revised arrangement and final decision come to hand):

|

Component |

Proposed access arrangement |

Draft decision |

Revised access arrangement |

Final decision |

|

Total revenue requirement |

$169.8m |

$129.7m |

$170.2m |

$146.5m |

|

Reference tariff |

$0.7596/GJ |

$0.5778/GJ |

$0.7605/GJ |

$0.6513/GJ |

|

Nominal risk free

rate |

5.48% |

5.53% |

5.54% |

5.53% |

|

Inflation forecast |

2.50%/yr |

2.57%/yr |

2.57% |

2.55% |

|

Real risk free

rate |

2.66% |

2.89% |

Not stated |

Not stated |

|

Cost of debt |

10.94% |

9.32% |

10.14% |

9.33% |

|

Debt risk premium |

5.46% |

3.79% |

4.60% |

3.80% |

|

Cost of equity |

11.98% |

10.335% |

12.04% |

10.33% |

|

Equity beta |

1.00 |

0.80 |

1.0 |

0.80 |

|

Market risk

premium |

6.50% |

6.00% |

6.50% |

6.00% |

|

Gearing |

60% |

60% |

60% |

60% |

|

Nominal vanilla WACC |

11.36% |

9.72% |

10.90% |

9.73% |

|

Opening capital base |

$112.4m |

$97.0m |

$102.7m |

$92.1m |

|

CapEx |

$14.4m |

$13.9m |

$40.7m |

$21.0m |

|

OpEx |

$73.0m |

$58.6m |

$71.9m |

$71.9m |

This concludes Pipes & Wires examination

of the AGP until about early 2015, when it is expected that the groundwork for

the next reset will be laid.

Mergers

& acquisitions

Germany

– RWE sells Amprion

Introduction

Pipes

& Wires #86 examined the formation of RWE’s UHV transmission grid

business RWE

Transportnetz Strom into a fully functional enterprise called Amprion GmbH, and hypothesised that this was

the first step of a sell-down that reflected a migration of RWE’s capital away

from lines and into energy. This article examines RWE’s recent sale of a 74.9%

stake in Amprion.

Details

of the transaction

A consortium of insurance companies and

pension funds led by Commerz

Real AG will ultimately buy a 74.9% stake in Amprion based on an enterprise

value of €1.3b. This represents most of Amprion’s RAB, and an EBITDA ratio of

about 8. This will relieve RWE of much of the expected €3b of renewal and

growth CapEx planned for the next 10 years.

RWE’s

strategy

A major part of RWE’s strategy is to

off-load about €8b of assets over the next few years to strengthen the balance

sheet, and, like several other European giants, the sell off is focusing on

grids and networks reflecting a migration of capital to unregulated energy

activities which are considered to be a better investment in the face of a lot

of CapEx and tightening regulation.

Similar

grid sales

This deal represents a continuation of the

trend set by E.On’s sale of its 380kV and 220kV transmission grid business Transpower

Stromübertragungs GmbH to state-owned

Dutch transmission utility TenneT

(refer to Pipes

& Wires #88).

Germany

– will EnBW sell its’ grid ?

Introduction

On the back of a flurry of grid sales in

Germany, this article examines EnBW’s recent announcement

that it is willing to sell a minority stake in its transmission grid business.

EnBW’s

transmission business

EnBW Transportnetze AG (TNG) comprises 3,645km of 380kV and

220kV grids across southern Germany. About 80 substations interconnect TNG with

local 110kV lines and other grid operators such as Amprion, TenneT and SwissGrid. Like many grids, TNG has a high

CapEx forecast, prompting EnBW to consider selling a stake to mitigate its exposure

to that CapEx. The recently elected Green government of Baden-Wuerttemburg

has suggested that the proceeds be used to invest in renewables and gas-fired

generation.

Potential

buyers

So who might be interested in buying a

minority stake in TNG ? Possibilities include...

·

A

group of local (German) pension funds or insurance companies that have an

appetite for the low risk and the reasonably certain cash returns that a

regulated grid business provides.

·

A

group of German cities or states.

·

A

wider group of investors (such as middle-east wealth funds or Australian

banks), possibly in conjunction with a European grid operator.

·

Specialist

utility investors such as Cheung Kong

Infrastructure.

·

A

European grid operator.

Given that any stake sold is likely to be

fairly small relative to other similar deals, it would seem to rule out the

interest of global groups or specialist utility investors. TNG’s location in

southern Germany could make it strategically significant to other utilities in

terms of connecting low-cost markets (like the TenneT deal described in Pipes

& Wires #88), however that could encounter anti-trust concerns. Given that

TNG is already 45% owned by the state of Baden-Wuerttemburg and 45% owned by

local cities, state ownership of a separated TNG would seem unlikely.

Likely

sale price

Some very simplistic analysis of recent

grid sales indicates sale prices between €80,000 and €150,000 per line km,

which suggests that even a 49% stake in TNG could sell for somewhere between

€140m and €270m. That’s certainly not a huge transaction amongst the scale of

what we’ve observed recently.

So ... anyway ... enough speculation. We

will just have to wait and see what emerges. Pipes & Wires will comment

further as and when a deal unfolds.

Energy

markets

Europe

– RWE and Gazprom form joint venture

Introduction

There is little doubt that most if not all

of Europe’s future gas supply will come from Russia. This article examines a

recently announced joint venture between German electric utility RWE and Russian gas supplier OAO Gazprom to build gas-fired generation

across Europe.

The

impending security of supply crisis

Many individual countries in Europe are

facing a security of electricity supply crisis. Some of the key drivers

include....

·

Shutdown

of coal-fired plants due to dwindling coal mining capability and pressure to reduce

CO2 emissions.

·

The

end of indigenous gas reserves such as the North Sea fields that supplied the

UK.

·

A

reliance on insecure renewable generation.

·

The

expected decommissioning of many older nuclear stations (such as the Magnox

stations in the UK).

·

More

recently, a slowdown of France’s nuclear construction program.

The recent policy shift in Germany (refer

to Pipes

& Wires #102) following the Fukushima earthquake in Japan will result

in the staged shutdown of Germany’s nuclear plants (much of which will impact

on RWE), leaving a further hole in Europe’s secure generation.

The

joint venture

The joint venture will form a company

focused on existing and new gas-fired (and hard coal-fired) generation in

Germany, Belgium, Holland, Luxembourg and the UK. It appears that RWE will

bring the electricity generation expertise to the joint venture, while Gazprom

will supply the gas. RWE has publicly denied that Gazprom would buy a stake in

RWE that would be of the nature of a bail-out.

Gazprom’s

strategy

Part of Gazprom’s strategy is to increase

its exposure to electricity generation in western Europe (long-time readers

might have spotted this trend amongst gas suppliers). Germany’s recent decision

to shut down its’ nuclear stations has provided a perfect opportunity for

Gazprom to meet a sudden gap in the market.

Competition

considerations

Understandably the cooperation of 2 very

large market players has raised the distinct possibility of anti-trust

concerns, and indeed the Bundeskartellamt

has indicated that it will be closely examining the joint venture.

This joint venture is likely to provide a

heap of good stuff for Pipes & Wires to examine – strategy, energy markets,

competition law, regulation, energy policy etc. So be prepared for some

extensive analysis over the next few months !!!

Industry

restructuring

Germany

– selling the grids (summary)

Sale of transmission grids in Germany has

been a recurring theme of Pipes & Wires over the last 2 years. This article

quickly summarises those deals....

|

Grid assets |

Line length |

Seller |

Buyer |

Price |

Stake |

Strategy |

|

RWE

Transportnetz Strom (Amprion) |

11,000km |

German pension funds and insurance

companies. |

€1.3b |

74.9% |

Migrate capital away from lines to

energy, avoid future CapEx. |

|

|

10,700km |

Dutch grid operator TenneT. |

€1.1b |

100% |

Migrate capital away from lines to

energy, avoid future CapEx. |

||

|

9,700km |

Belgian grid operator Elia (60%), Australian funds manager IFM

(40%). |

€810m |

100% |

Migrate capital away from lines to

energy, avoid future CapEx. |

||

|

3,645km |

No sale confirmed yet. |

|

Minority |

Avoid future CapEx, possibly migrate

capital to renewables or gas-fired generation. |

Philippines

– privatisation surges ahead

Introduction

The Philippines is a country most of know

little about. This article examines the recent progress on electricity reform

and restructuring that has been in progress since 2001.

The

original industry structure

Like many other countries with state-owned

electric systems, the Philippines system was dominated by the

vertically-integrated National Power

Corporation (Napocor) which was established in 1936. In 1978 Napocor

concluded the purchase of metro Manila’s supplier MERALCO’s generation plants, leading to a

single, nation-wide integrated generation utility. In 1988 Napocor further

purchased the small generation plants in all other areas.

The

reform process

Vertical disaggregation of the industry was

foreshadowed in 1998 by the Omnibus Power Bill which (not surprisingly) did the

following....

·

Disaggregated

Napocor into 7 competing generation companies that would be prohibited from

owning either transmission or generation.

·

Formation

of a separate open-access transmission grid business.

·

Establishment

of regulated distribution companies, with the added features of having

protected distribution areas but also having supplier-of-last-resort

obligations.

·

Establishment

of spot and bilateral contract markets.

·

Formation

of a government entity to own all the assets and liabilities that

were likely to be unsustainable in a competitive market, to be known as Power Sector Assets &

Liabilities Management (PSALM).

A

few hiccups along the way

Like most reform and privatisation

processes, there is usually a strong tension between the potentially

conflicting objectives of maximising the sale price on one hand, and protecting

consumer interests on the other hand. This was perhaps more of an issue in the

Philippines were populist politicians had kept electricity tariffs low by government

decree, which not surprisingly has led to significant under-investment.

Recent

progress

Recent softening of regulatory policy and

sweetening of the investment incentives, have however, strengthened the

interest of private investors to the point where over 33% of the market

capitalisation of the Philippines Stock

Exchange is from electric companies. Some of the private investors involved

so far include...

·

Former

brewery San Miguel now owns 4

generation plants and a 33% stake in MERALCO.

·

A

consortium comprising OneTaipan, Calaca High Power Corporation and the State Grid Corporation of China

has been awarded a 25 year concession to operate the National Grid.

·

Abolitz Power Corporation has bought

out its’ partner in the Luzon

Hydro Corporation.

It appears that the private sector’s

interest will continue, especially on the back of the Energy Regulatory Commission’s approval of

PHP5b (about US$117m) of new projects.

Regulatory

policy

UK

– determining the efficient expenditure

Introduction

Pipes

& Wires #103 examined the Office of Rail Regulation’s Periodic Review

2013 (PR13) that will shape the 5th rail Control Period (CP5)

starting on 1st April 2014 (with a yet-to-be-determined end date).

This article examines a paper entitled “determining the

efficient expenditure” released as part of PR13, and also considers it in

the wider context of pipes & wires businesses.

A

few key background issues

Network

Rail’s turbulent birth out of the Hatfield accident and the subsequent

placing of Railtrack PLC into

administration in 2002 resulted in the annual OpEx and Renewal CapEx increasing

from £3.9b to £7.2b over a 2 year period to address a significant back-log.

However, addressing this back-log came at the expense of declining efficiency.

CP3 (1st April 2004 to 31st March 2009) expected a 31%

efficiency improvement, and while Network Rail was able to achieve a 27%

efficiency improvement it struggled to deliver on the track renewal program.

Subsequently, CP4 (1st April

2009 to 31st March 2014) expected a further efficiency improvement

of 21% which, in contrast to CP3, was allowed to claim a reduced volume of

renewal work as an efficiency gain (as distinct from just unit cost

improvements).

Key

features of the “determining the efficient expenditure” paper

The key features of ORR’s paper include....

·

A

reiteration that Network Rail’s proposed CP4 spend of £35.1b would be reduced

to £32.2b by a requirement to generate inter

alia cost efficiencies of 21%.

·

A

reiteration of ORR’s approach of assuming efficiency improvements and then

incentivising Network Rail to out-perform that assumption, rather than

specifying a minimum efficiency gain.

·

A

recognition that Network Rail’s devolution of management and granting

infrastructure management concessions to third parties will require a different

regulatory approach.

·

A

fairly standard mix of building block assessments, including bottom-up analysis

of work volumes, benchmarking of unit costs, a top-down analysis to support the

overall picture, and a view on the likely efficiency gains that could be made.

ORR’s general approach

ORR has indicated that its’ general approach to

setting CP5 will include....

· A more geographically disaggregated analysis

by route lines rather than just by England & Wales, and Scotland.

· A greater focus on bottom-up analysis.

· Include wider benchmarking cohorts, such as

the global rail sector and specific tasks.

· Giving greater attention to exploring the

drivers of efficiency gaps (presumably to determine whether further efficiency

gains are feasible).

· A continued refining of the information

disclosure requirements applicable to Network Rail.

· A greater scrutiny of Network Rail’s asset

management processes and practices.

ORR’s specific approach to assessing likely efficiency gains

In assessing the likely efficiency gains, ORR has

considered the following 2 dimensions....

·

Catch-up

efficiency gains, wherein Network Rail will be encouraged to achieve the

efficiency levels of the most efficient operators in the benchmarking cohort.

·

Frontier

shift efficiency gains, wherein the most efficient operators in the

benchmarking cohort will be expected to make further continuous improvements.

Considering

the elements of “determining the efficient expenditure” in the wider pipes

& wires context

On the whole, the paper shows a continual

refining of the building blocks approach, but certainly nothing exceptional nor

anything that is significantly ahead of other pipes & wires regulators.

Having said that, ORR are to be commended for intending to place a greater

emphasis on bottom-up analysis and for intending to more closely examine the

drivers of efficiency gains and gaps.

Pipes & Wires will comment further as

the PR13 process progresses.

Energy

policy

US

– recharging electric cars

Introduction

Pipes

& Wires #98 noted that Dominion Resources

was seeking approval from the Virginia

State Corporation Commission to introduce a voluntary tariff that

encourages off-peak recharging. This article examines the VSCC’s decision.

The key issues

I

don’t think it would be unfair to say that the whole issue of recharging

electric cars is poorly understood by both the wider community and by many

policy makers. In particular, the whole need for electric cars to recharged at

off-peak times seems poorly understood (and in many countries even off-peak

recharging will still be with fossil-fired plants, so it will only result in

avoiding new generation capacity, not the emissions).

Dominion’s

proposed recharging tariff

The basis of Dominion’s recharging tariff

is the 10pm to 6am off-peak period. Dominion has proposed a price of $0.34 to

recharge a car sufficient for 40 miles (this much electricity would normally

cost about $0.86), whilst also proposing to charge $1.23 for a similar recharge

during peak periods.

Dominion has projected 86,000 electric cars

in Virginia alone by 2021, which would require an extra 270MW of generation

capacity if recharged at peak times.

Key

aspects of the VSCC’s decision

The VSCC approved Dominion’s plan in July

2011. Key aspects of that decision include...

·

Up

to 750 customers will be able to sign up for the pilot project from 3rd

October 2011, and must stay with the project for at least 1 year.

·

An

“electric vehicle only” option, in which Dominion estimates a price of $0.41 to

recharge for a 40 mile commute. This has a circuit supplied from a 2nd

meter.

·

A

“whole house” option that encourages other household activities to be shifted

to off-peak periods, whilst imposing a higher rate for peak periods.

The pilot project will conclude on 30th

November 2014, over which period Dominion will be reporting to the VSCC on

uptake rate and the emerging feasibility of a wider scheme.

A bit of light reading…

Wanted – old electricity history books

If

anyone has an old copy of the following books (or any similar books) they no

longer want I’d be happy to give them a good home…

·

White Diamonds North.

·

Northwards March The Pylons.

·

Two Per Mile.

·

Live Lines (the old ESAA journal)

Conferences & training courses

The following

conferences and training courses are planned...

·

Infrastructure:

Investment & Regulation – Sydney, 21st October, 2011.

·

Fundamentals

of the NZ electricity industry – Auckland, 26th – 27th

October, 2011.

·

Fundamentals

of the NZ electricity industry – Wellington, 9th – 10th

November, 2011.

·

Fundamentals

of the NZ electricity industry – Wellington, 8th – 9th

May, 2012.

·

Fundamentals

of the NZ electricity industry – Auckland, 22nd – 23rd

May, 2012

Opt out from Pipes & Wires

Pick

this link

to opt out from Pipes & Wires. Please ensure that you send from the email

address we send Pipes & Wires to.

Disclaimer

These articles

are of a general nature and are not intended as specific legal, consulting or

investment advice, and are correct at the time of writing. In particular Pipes

& Wires may make forward looking or speculative statements, projections or

estimates of such matters as industry structural changes, merger outcomes or

regulatory determinations.

Utility

Consultants Ltd accepts no liability for action or inaction based on the

contents of Pipes & Wires including any loss, damage or exposure to

offensive material from linking to any websites contained herein.

{kind=link}