From the editor’s

desk…

Welcome

to Pipes & Wires #102. Once again our thoughts and prayers are with our

clients and friends in Christchurch after yet more earthquakes.

This

issue covers a wide range of issues, including the rapidly unfolding regulatory

framework for electricity lines and gas pipelines in New Zealand, the rapidly

shifting nuclear policy in Germany, and a broad overview of mergers and

industry reshuffling in North America.

Accredited supplier status

Utility

Consultants is pleased to announce that it is now an Asia-Pacific Utilities Group (APUG) accredited

supplier (registration number 88899493).

Get Pipes & Wires “white-listed”

To

avoid being intercepted by your server as spam, please arrange to have phil.caffyn@utilityconsultants.co.nz

“white-listed” by your IT people.

Pipes & Wires on the web

Pipes & Wires on Linked In

Pipes

& Wires now has an on-line

group for readers to keep in touch on a more regular basis, bounce ideas

around or raise issues and concerns. Pick here

to visit my Linked In profile and add me

to your connections.

Pipes & Wires on Facebook

Pipes

& Wires now also has its own Facebook

page. Just go to Facebook’s home page and search for Pipes & Wires.

Pipes & Wires on YouTube

To

see a short video clip explaining more about Pipes & Wires, pick here.

Pipes & Wires on the web

To

read more about Pipes & Wires, pick here.

About Utility Consultants

Utility

Consultants Ltd is a management consultancy specialising in pretty much all aspects of energy and infrastructure

networks – pick here

to see more, or to be sent a detailed profile of recent projects, pick

here.

Asset

strategy

NZ

– public safety management systems

Just a reminder that the requirement for

all electricity businesses (of more than 10MW capacity) to have their PSMS in

place and externally audited is only 9 months away. For help with compiling

your PSMS, or to have a pre-audit review undertaken, phone Phil on (07)

854-6541 or pick

here.

UK

– redesigning the pylons

Introduction

The overall shape of high voltage pylons

has changed little since the 1920’s. This article examines a competition being

held by National Grid to identify

new shapes for pylons in the face of a lot of new build to connect wind farms

and the new nuclear stations.

Background

Pylon design has changed little from the

utilitarian design of the mid-1920’s. Those who got the chance to watch the 1st

episode of “The Secret Life Of The National Grid” (before it was removed from

You Tube) may have noticed the UK’s concern about the harsh, brutal appearance

of pylons in countries that were considered to have a higher degree of state

intervention (which apparently conservative Prime Minister Stanley Baldwin was

keen to avoid). To this end, the Central

Electricity Board engaged the famed architect Sir Reginald Blomfield

to design something less intrusive, and less representative of state intrusion

and power. Over the next 85 years some 88,000 pylons were built.

The

competition

A competition is being run by the Royal

Institute of British Architects on behalf the Department of Energy and Climate

Change and National Grid to identify designs that will, in the words of Energy

Secretary Chris Huhne “accommodate infrastructure into our natural and

urban landscapes”. The competition closes on the 12th July and the

entries will be displayed at the London Design Festival in September. Pipes

& Wires will revisit this issue around that time to see what the entrants

have come up with.

US

– joining forces for regional grid development

Introduction

The need to “invest” in electricity

transmission grids seems to become ever more pressing, despite the apparent

easing of the high demand growth experienced a few years ago. This article

briefly examines a joint venture between 2 giant US utilities to coordinate

grid investment, but firstly we set out a few thoughts on grid CapEx.

A

few thoughts on grid CapEx

Transmission grids are under 3 dimensions

of spend “pressure” (and there are similar parallels for gas transmission

pipelines as well):

·

Renewal

CapEx - the need to renew or replace existing lines simply because their

condition has declined to the point where Renewal CapEx is cheaper and more

reliable than continued OpEx (and if anyone wants to talk about this,

especially in the Australian and New

Zealand regulatory context, please

pick here).

·

Growth

CapEx - the need to increase the capacity of existing lines due to demand

growth or re-determined security of supply requirements.

·

Extension

CapEx - The need to build new lines in completely new areas to import

electricity from new generation sites (typically remotely sited wind farms).

For a more detailed explanation of these

terms, pick here.

The

joint venture

A non-binding MOU has been signed between American Electric Power (AEP) and the Tennessee Valley Authority (TVA) to

collaboratively identify mutually beneficial EHV transmission opportunities

along the boundary of the PJM and TVA grids.

It would seem that a key benefit of a joint approach would be avoiding

duplication, and therefore enhancing allocative efficiency (obviously a key

goal of regulators).

In addition to this MOU, AEP in conjunction

with Duke Energy has

entered into a separate MOU with the TVA to build 55 miles of 765kV line

between Rockport Power Station, Indiana and Paradise Power Station in Kentucky.

It will be interesting to see how the FERC

and the various state regulators treat these joint approaches, so Pipes &

Wires will check back in a couple of months.

NZ

– progress on the NIGUP

Work on the NIGUP (known to many of

us the 400kV) seems to be proceeding well. Those that like looking at power

lines might have noticed a few towers without wires (which is a pretty

interesting sight) but along Highway 1 at Karapiro are several monopoles

without conductors which look so cool against a grey sky. For those in the

South Island, they look very similar to the 220kV monopoles near Carisbrook on

the Three Mile Hill – South Dunedin line.

Mergers

& acquisitions

US

– Fortis enters the regulated US market

Introduction

Mergers consolidating the US electricity

distribution industry have been a common theme of the last few issues of Pipes

& Wires. This article examining Fortis’ acquisition of the Central Vermont Public Service Corp (CVPSC) sort

of follows that theme, albeit with a few differences.

Who

are the deal partners ?

The deal partners are:

·

Fortis

is Canada’s largest investor-owned distribution utility, with 2,300,000

regulated electric and gas customers in Canada and the Caribbean as well as

hydro in Canada, the Caribbean and the US. One of their objectives is to

achieve a return on capital commensurate with that of a well-run North American

utility.

·

The

CVPSC is a publicly listed utility supplying 159,000 customers throughout the

US state of Vermont, and also owns a 41% stake in Vermont Transco LLC (which

owns and operates Vermont’s high-voltage grid).

The

proposed deal

Fortis will acquire CVPSC for $470m in cash

and the assumption of $230m in debt. The cash offer of $35.10 per share

represents a premium of about 44% above CVPSC’s closing price on the NYSE,

which is significantly higher than the premiums paid in other recent deals.

Like most other deals, this is subject to approval by the Vermont Public Service Board

and the FERC.

Fortis has indicated that the key reasons

for acquiring CVPSC include the acquisition being accretive to EPS within 1

year, and a cost-of-service regulatory regime that is stable, has minimum lags,

and allows pass through of key inputs such as fuel, transmission charges and

energy purchases.

Pulling

together some wider thoughts

Some of the reasons for recent mergers in

the US have included:

·

The

need to extract operating efficiencies in the face of increasing costs.

·

The

need to better utilise generation and transmission by capturing geographical

diversity.

·

The

need to capture higher retail margins in an era of languishing wholesale prices

(the AES – DPL acquisition).

·

The

need to migrate capital from distribution to transmission where higher returns

are allowed (refer to Pipes

& Wires #97 where National Grid

sold its 2 regulated New Hampshire businesses to a Canadian utility).

Being a portfolio investor, Fortis motivations

may be somewhat different than the other mergers that have been examined, with

the allowable return being a likely significant driver.

Canada

– investing in the US

Introduction

Pipes

& Wires #97 noted that Algonquin Power & Utilities Corp’s

acquisition of National Grid’s Granite

State Electric and EnergyNorth businesses might represent another emerging

wave of investment. Fortis’

acquisition of the Central Vermont Public

Service Corporation could represent another chunk of that wave, which is

what this article examines.

What constitutes an investment wave ?

It’s

hard to define, but I guess an investment wave could be defined as a

“reasonable number of separate investments from the same jurisdiction to the

same jurisdiction for similar reasons over a reasonably distinct period of

time”. I think it would be pushing it to infer that 2 deals worth less than $1b

constitutes a wave, but it may represent the start of a wave.

Summary of the 2 deals so far

The 2 deals so far can be summarised as:

|

Deal |

Consideration |

|

Algonquin

acquisition of Granite State and EnergyNorth. |

$285m

cash. |

|

Fortis

acquisition of Central Vermont. |

$470m

cash, $230m debt assumption. |

This could be the beginning of something,

especially if individual US states begin allowing higher returns to discourage

capital migrating to FERC-regulated transmission grids.

US

– approving the Duke – Progress merger

Introduction

Pipes

& Wires #100 examined Duke

Energy’s pursuit of Progress

Energy, and noted that the approval of both the North

Carolina Utilities Commission and the South

Carolina Public Service Commission is required (as well as the approval of

several other regulators such as the DoJ

and the FERC). This article examines Duke’s

attempt to circumvent the SCPSC’s approval requirement by merging only Duke and

Progress’ holding companies but not the operating subsidiaries.

The

key issue

Duke and Progress plan to firstly merge

only the holding companies, and then several years along the track merge the

operating companies (that will release most if not all of the merger

synergies). Duke believes that South Carolina law gives the SCPSC jurisdiction

only over the merger of operating companies, not of corporate owners.

The

regulator’s responses

The SCPSC is understandably arguing that it

should be able to rule on the deal as it affects electric and gas customers in

South Carolina, whilst the NCUC has allowed

the South

Carolina Office Of Regulatory Staff to participate in hearings in North

Carolina as a party of record.

Given the flurry of merger activity, this

approach could well prove very valuable to the industry, so Pipes & Wires

will watch this one closely. Thanks to Spiegel

& McDiarmid LLP in Washington, DC for their assistance with this

article.

Energy

policy

Germany

– phasing out the phase out of the phase out

Introduction

The 3 months or so since the Japanese

earthquake have precipitated a significant shift in the way Germany views

nuclear power. This article revisits the policy shifts and then examines the

latest policy and its implications.

The

policy shifts to date

German nuclear energy policy has taken the

following shifts:

·

Back in 2000 the German coalition

government announced its intention to phase out nuclear power. This intention

was subsequently enacted as the Nuclear Exit Law and has already seen plants at

Stade, Obrigheim

and Krummel closed down in November 2003, May 2005 and June 2007 respectively. The

30 year old plus stations at Biblis, Neckarwestheim

and Brunsbüttel

were scheduled for closure in 2010, which would have removed about 5,540MW of

Germany’s 120,000MW of installed capacity.

·

In 2005 a new federal government was

elected in which Chancellor

Angela Merkel announced an intention to re-negotiate the required closures.

However her party’s coalition agreement with the Social

Democrat Party (SPD) saw the closure policy being retained for the time

being.

·

In early 2008 Merkel and her party

shifted to an open opposition of the nuclear phase-out and rejected a

compromise by the SPD to postpone further shutdowns in return for a ban on new

nuclear plants. Media comment suggested that the SPD were on the way out in the

build up to the 2009 election as public opinion shifted toward “phasing out the

phase out” (but appeared to stop short of approving new nuclear stations).

·

After

the 2009 election little time was lost in reaffirming the

coalition government’s taste for nuclear energy, with a formal statement

emerging from the CDU that Germany needed nuclear energy as a bridge until

renewable are able to fill the gap.

·

The radiation leaks from Fukushima

prompted vigorous protests from the anti-nuclear brigade, but also prompted something

of a quick policy U-turn by Merkel who announced that last year’s life

extension decision of 17 plants has been suspended for 3 months, and that

shutdown of the 7 oldest reactors will proceed.

The

latest pronouncements

Key aspects of the Merkel government’s

latest policy are:

·

Closure

of all nuclear plants by 2022.

·

Reduce

electricity consumption by 10% by 2020.

·

Increase

the contribution of renewables to 35% by 2020.

·

Possibly

scrapping a tax on fuel rods (worth about €2b per year to the government) in

return for the utility industry supporting an early phase-out.

Some commentators have described Merkel’s

plans as being more green than the Greens, whilst the heavy industrial sector

is reiterating its concerns about security of supply and the already-high

prices and the union representing nuclear plant operators is warning that

“thousands of jobs will be lost”.

The

likely implications

Nuclear represents about 23% of Germany’s

annual 595,000 GWh of (gross) generation. Given the pressure to also reduce

coal-fired generation (aside from the simple issue of plant aging and

retirement) and the heightened tensions around gas supply from Russia, close to

80% of Germany’s electricity generation could be considered insecure or of

limited life. So if Germany can achieve

the desired 10% reduction in consumption and 35% renewables, they might just

squeak home (that is if they continue with the current levels of coal and

gas-fired generation).

Regulatory

decisions

NZ

– the next gas distribution price reset

Introduction

The current regulatory framework for gas

pipeline businesses requires the Commerce

Commission to set an initial default price-quality path (Initial DPP) as

soon as practicable after 1st July 2010. This article examines the Discussion

Paper that was released in April (and has since been extensively consulted

upon).

The

regulatory framework

The broad regulatory framework is set out

in Part

4 of the Commerce Act 1986, and in particular the following subparts are

directly relevant to gas pipeline businesses:

·

Subpart

3 – Input Methodologies.

·

Subpart

4 – Information Disclosure regulation.

·

Subpart

6 – Default and Customised Price-Quality Path regulation.

·

Subpart

10 – Gas Pipeline Services.

Key

work to date

A major work stream to date has been

compiling the Input Methodologies pursuant to Subpart 3, which was completed in

December 20101. The Discussion Paper sets out the Commission’s thinking on

aspects of the DPP that are not prescribed in the Input Methodologies such as

setting appropriate price paths, rates of change, quality standards, regulatory

control periods and compliance assessment periods.

Commission’s

current views on key parameters

The Commission’s current views include inter alia:

·

Gas

transmission and distribution should be treated differently.

·

A

weighted average price cap is considered the most suitable form of control for

gas distribution and for Vector’s gas transmission, whilst a total revenue cap

is considered the most appropriate for Maui Developments.

·

The

compliance mechanism is likely to be an allowable notional revenue approach.

·

The

option of a Customised Price Path is considered a sufficient approach for

accommodating the future investment needs of a gas transmission business.

·

An

X-factor of 0 is considered appropriate for the Initial DPP.

·

The

key quality standard to be incorporated into the Initial DPP is safety, and it

is expected that other quality parameters will be scrutinised through the

Information Disclosure process and may be used to include quality measures in

future DPP’s.

·

The

preferred regulatory period will be for 4 years and 3 months, starting on 2nd

July 2012.

Next

steps

The Commission expects the following next

steps:

·

The

possibility of an updated Discussion Paper in late August, with consultation

through to late October 2011.

·

Draft

decisions paper and draft determination in early December, with consultation

through to late January 2012.

·

Final

reasons paper and final determination in late February (pending confirmation of

the Initial DPP starting on 2nd July 2012).

Pipes & Wires will make further comment

as the discussion papers and decisions emerge.

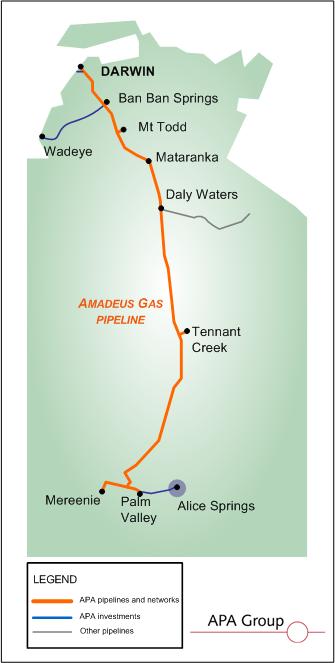

Aus

– revised AGP access arrangement

Introduction

Pipes

& Wires #101 discussed the Australian

Energy Regulator’s (AER) recent draft

decision to not accept NT Gas’

proposed access arrangement for the Amadeus Gas Pipeline (AGP)

for the regulatory period from 1st July 2011 to 30th June

2016. This short article examines NT Gas’ revised access arrangement

The

revised access arrangement

The following table compares the AER’s

draft decision with NT Gas’ proposed access arrangement (and will be completed

as the revised arrangement and final decision come to hand):

|

Component |

Proposed access arrangement |

Draft decision |

Revised access arrangement |

Final decision |

|

Total revenue requirement |

$169.8m |

$129.7m |

$170.2m |

|

|

Reference tariff |

$0.7596/GJ |

$0.5778/GJ |

$0.7605/GJ |

|

|

Nominal risk free

rate |

5.48% |

5.53% |

5.54% |

|

|

Inflation forecast |

2.50%/yr |

2.57%/yr |

2.57% |

|

|

Real risk free

rate |

2.66% |

2.89% |

Not stated |

|

|

Cost of debt |

10.94% |

9.32% |

10.14% |

|

|

Debt risk premium |

5.46% |

3.79% |

4.60% |

|

|

Cost of equity |

11.98% |

10.335% |

12.04% |

|

|

Equity beta |

1.00 |

0.80 |

1.0 |

|

|

Market risk

premium |

6.50% |

6.00% |

6.50% |

|

|

Gearing |

60% |

60% |

60% |

|

|

Nominal vanilla WACC |

11.36% |

9.72% |

10.90% |

|

|

Opening capital base |

$112.4m |

$97.0m |

$102.7m |

|

|

CapEx |

$14.4m |

$13.9m |

$17.5m |

|

|

OpEx |

$73.0m |

$58.6m |

$71.9m |

|

Pipes & Wires will make further comment

as the final decision emerges.

NZ

– electricity distribution starting price adjustments

Introduction

Non-exempt

electricity distribution businesses have been subject to a default

price-quality path (DPP) since April 2010. The regulatory framework provides

for the Commerce Commission to reset

that DPP if the recently developed Input Methodologies would have resulted in a

materially different DPP had they applied in April 2010. This article examines

the Commission’s Starting

Price Adjustment (SPA) paper that was released back in April 2011 (and has

since been consulted on).

The

regulatory framework

The operative component of the regulatory

framework is s54K(3)

of the Commerce Act 1986 which states “If an input methodology is published after

1 April 2010 and if, had that methodology applied at the time the default

price-quality paths were reset as required by subsection (1), it would

have resulted in a materially different path being set, then the Commission may

reset the default price-quality paths in accordance with section 53P and may apply claw-back,

despite section 53ZB(1)”.

Key

issues in the SPA paper

The principle issue addressed in the SPA

paper is the Commission’s proposal to reset starting prices for the 2010 – 2015

regulatory period based on the current and projected profitability of distribution

businesses. A few of the key issues set out in the SPA paper include:

·

The

Commission’s proposal to set starting prices so that businesses may be expected

to earn at least a normal rate of return over the regulatory period given

assumed industry-wide trends.

·

In

the event that the industry-wide assumptions do not provide adequate returns,

the Commission considers that the option of applying for a Customised Price

Path provides an adequate remedy.

·

The

Commission notes that the Commerce Act provides it (the Commission) with

discretionary powers to apply claw-back at the time of resetting the DPP

starting prices.

This is obviously a significant issue for

the distribution businesses, so Pipes & Wires will comment as the

Commission’s thoughts emerge.

NZ

– exempting the Sidewinder Pipeline

Introduction

Schedule

6 of the Commerce Act 1986 lists the pipelines that are exempt from the

requirements of Part

4 of the Commerce Act 1986. This article examines the Commerce Commission’s Proposed Recommendation

to the Minister of Energy that TAG

Oil’s Sidewinder Pipeline be added to that Schedule ie. exempted from the

requirements of Part 4.

The

Sidewinder Pipeline

Sidewinder is a dedicated 200mm nominal

diameter gas transmission pipeline that will stretch about 3.35km from TAG

Oil’s Sidewinder field in the Taranaki Basin to an interconnection point on Vector’s

high pressure transmission pipeline.

Legal

aspects to recommending exemption

Sidewinder’s current regulatory status (the

default) is that it is automatically subject to the Information Disclosure

requirements and Price-Quality regulation under Part 4. However s55A(6)

of the Act provides for the Minister to recommend exemption (ie. addition to

Schedule 6) if inter alia the owner

of the pipeline does not have a substantial degree of market power.

Key

aspects of the Proposed Recommendation

In making its recommendation to the

Minister, the Commission has considered the following lines of thought:

·

TAG

Oil will only be transporting its own gas through Sidewinder therefore third

party access is not an issue, so TAG will only be providing pipeline services

to itself.

·

The

open access of both the Vector and Maui pipelines in Taranaki provides a single

market with highly transparent prices. TAG’s expected maximum injection into

that market is expected to be about 9% of the lowest ever recorded market

volume, hence TAG would be unlikely to be able to exert any market power.

The Commission will be consulting on its

recommendation around the time this issue is published, so Pipes & Wires

will check back in a few months.

A bit of light reading…

Wanted – old electricity history books

If

anyone has an old copy of the following books (or any similar books) they no

longer want I’d be happy to give them a good home…

·

White Diamonds North.

·

Northwards March The Pylons.

·

Two Per Mile.

·

Live Lines (the old ESAA journal)

Conferences & training courses

The following

conferences and training courses are planned...

·

Infrastructure:

Investment & Regulation – Sydney, 21st October, 2010.

Opt out from Pipes & Wires

Pick

this link

to opt out from Pipes & Wires. Please ensure that you send from the email

address we send Pipes & Wires to.

Disclaimer

These articles

are of a general nature and are not intended as specific legal, consulting or

investment advice, and are correct at the time of writing. In particular Pipes

& Wires may make forward looking or speculative statements, projections or

estimates of such matters as industry structural changes, merger outcomes or

regulatory determinations.

Utility

Consultants Ltd accepts no liability for action or inaction based on the

contents of Pipes & Wires including any loss, damage or exposure to

offensive material from linking to any websites contained herein.

{kind=link}