Pipes & Wires

From the editor’s desk…

Welcome

to Pipes & Wires #204. This issue starts by examining the increasing need

for centralised coordination of power systems. We then examine some market and

pricing issues in Japan and the UK, and then look to some grid security issues

including designating generation as must-run.

We

then look at an electricity transmission tariff reset in Australia, and

conclude with some industry structural reshufflings in India and South Africa. So

… until next time, happy reading…

Subscribe to Pipes & Wires

If

you’re receiving this second-hand, pick this link to subscribe.

Recent client projects

Recent

client projects include…

· Providing an independent review of

asset condition and spend forecasts for a distribution company investor.

· Estimating the costs of DERMS

(distributed energy resource management system) penetration for distribution

feeders for a large US electric company.

· Identifying leading practices in

behind-the-meter activities (eg. batteries, solar, smart data, VPP’s etc) for a

large US electric company.

· Identifying key learnings from the

transformation of a Dutch electric, gas and heat company for a large US

electric company.

· Identifying best Australian practices

in EV charging for a large US electric company.

· Identifying key features of demand

management in the Australian NEM for a large US electric company.

· Compiling a pricing model to reflect

asset investment levels to transmission grid exit level rather than averaged

over the entire network.

· Identifying best practices in

grid-scale and community-scale batteries for an Australian distributor.

· Identifying best practices in EV

charging on behalf of an Australian distributor.

· Recommending amendments to a security

of supply standard to better reflect demand density.

· Identifying best customer engagement

practices on behalf of an Australian distributor.

· Development of an asset management

journey aligned to ISO 55001.

· Identifying learnings from the RIIO –

ED1 reset on behalf of an Australian distributor.

· Developing a smart metering strategy.

· Advising on likely available electrical

contractors.

· Undertaking a customer survey to

identify customer preferences for off-peak EV recharging.

· Developing a strategy for complying

with the related party transaction provisions.

· Advising on the regulatory implications

of an aging timber transmission pole fleet.

· Compiling some introductory thoughts on

digital transformation and blockchain.

· Facilitating a series of client

workshops to better understand asset information criticality and in-service

failure risk.

· Assessing the strength of asset

management practices.

· Reviewing recent AER decisions to

understand the expectations around asset management practices and methods.

· Reviewing the AER’s recent treatment of

network transformation expenditure.

· Compiling overhead conductor and wooden

cross-arm fleet strategies.

· Identifying the issues around

customer-owned lines on private land.

· Developing a risk-based tree trimming

strategy.

· Developing an EV charging strategy.

· Analysing transmission charges as a

percentage of total electric bills.

· Compiling a strategy for improving the

resilience of a sub-transmission network.

· Developing a best-practice guideline

for smart metering.

Cool multimedia stuff

Clean

electricity

Those with a liking for Brit Comedy might

appreciate Mrs Bucket’s

concern for clean electricity.

Asset

management and asset strategy podcasts

My colleagues at the UMS Group have put

together a series of podcasts on asset management and asset

strategy, including an

interview with me on how to make asset

management happen in small companies. This

has also been republished as a short

narrative.

Regulating

emerging technologies

Global –

increasing need for centralised coordination

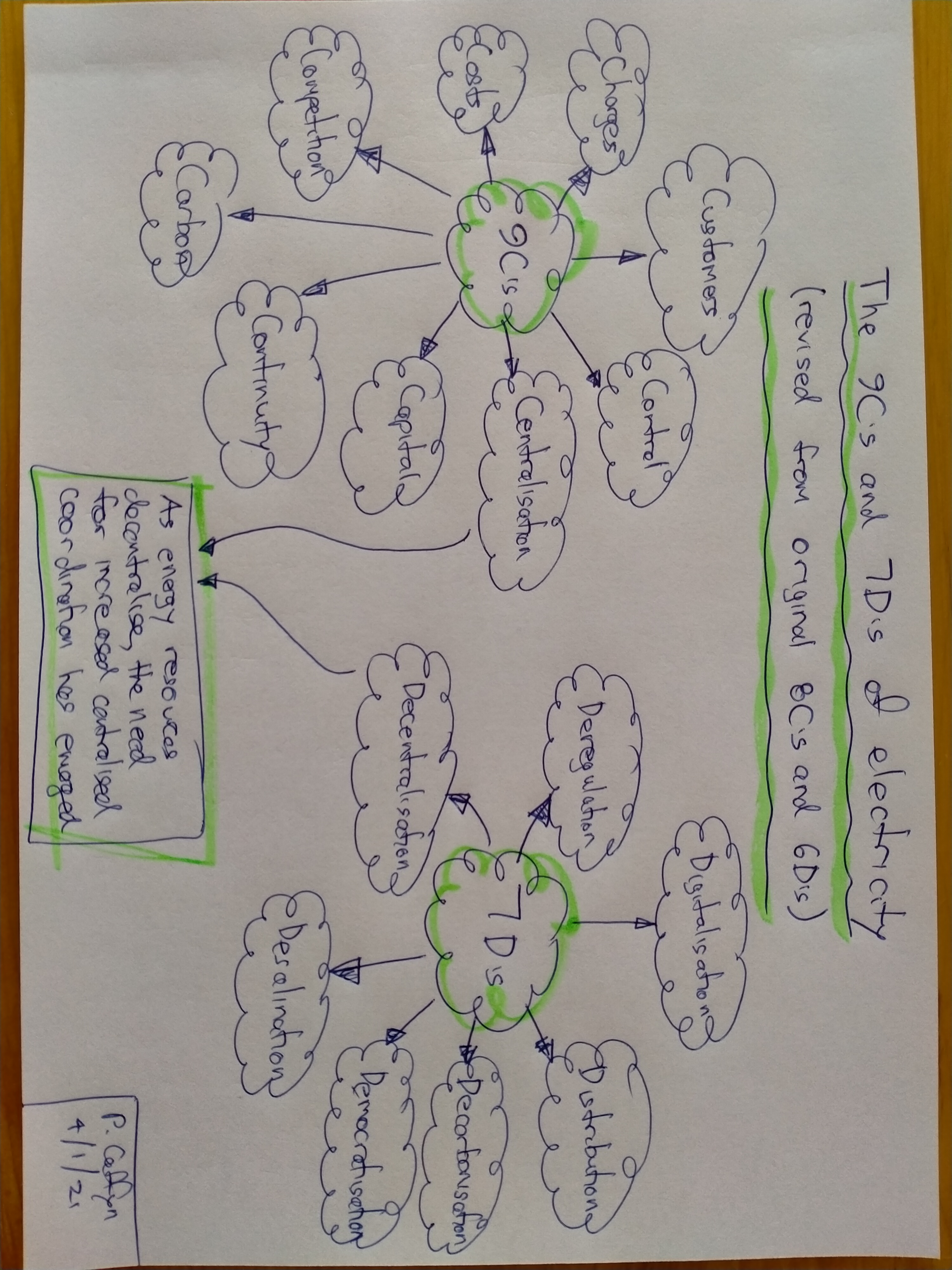

Introduction

Some readers might’ve seen the 8C’s and

6D’s model of the emerging electric company, in which 1 of the 6D’s is

decentralisation. This article presents an augmented 9C’s and

7D’s model along with some

topical examples illustrating how centralised coordination is becoming

increasingly important as energy resources decentralise.

The 7D’s

The 7D’s are…

|

· Digitalisation |

· Distribution |

· Decarbonisation |

· Desalination |

|

· Democratisation |

· Deregulation |

· Decentralisation |

|

It is worth noting that the recently

released consultants’

report for long-term water supply options for Auckland

includes desalination.

Examples

of centralised coordination

· Australia

– the establishment of a DER register to

provide visibility and centralised coordination of all DER’s at residential or

business locations.

· New

Zealand – the establishment of a Digital Twin by

Counties Power to better understand

how distributed functions such as solar, batteries and demand response effect

the network and provide customer benefits.

· California

– establishment of a central

procurement framework by the California

Public Utilities Commission to ensure local resource adequacy (the further step

of appointing PG&E and SoCalEd as the central procurement entities is of

concern to non-utility entities such as community aggregators).

The

strategic trend

At first glance this issue appears to be

one of tension between centralisation (C) and decentralisation (D), with

thoughts of which will win. Further thought suggests that they are in fact complimentary…

· Electric

grids have always had some degree of centralised control, certainly for the

last 100 years.

· Decentralisation

is a matter of perspective, because again generation sources have been

decentralised for the last 100 years. There are just now a lot more generation

sources, with most of them being smaller.

· Technology

has driven down the cost of monitoring and communication of pretty much

everything, making small generation viable.

Pipes & Wires will comment further as

this trend continues to emerge.

Energy

markets and pricing

Japan – examining

recent price rises

Introduction

It’s been a while since Pipes & Wires

has been to Japan (a bit over 6 years … Pipes

& Wires #140 in February 2015

actually). This article examines the recent government probe into surging

prices on the Japan

Electric Power Exchange (JEPX).

A bit

about the JEPX

Japan has the world’s fourth largest

electricity market, with annual generation of about 1,007,000 GWh (about 23x

New Zealand’s annual generation). The JEPX is a public interest incorporated

organization established in 2003 to facilitate both spot and forward

electricity market transactions. Most of Japan’s large electric companies and

electricity users are members of JEPX.

Recent

events

In early January 2021 spot prices rose for

the fourth day in a row, jumping to a record high of ¥103 per kWh as

colder-than-expected weather coincided with constrained gas supply to power

stations (for comparison, the average price for the 2020 year was ¥6.5 per kWh),

which was subsequently compounded by generation shutdowns following an

earthquake. Mitigations included the system operator OCCTO

instructing generators increase generation and to route as much energy as

possible to Tokyo and Osaka.

The

government probe

The Electricity & Gas Market Surveillance

Commission (EGC) is examining

whether speculation and deliberate withholding of generation from the JEPX has

contributed to the price spiking. Initial conclusions are that there were no

obviously improper trades, and that LNG shortages constrained gas-fired

generation.

UK – sixpence

anytime EV charging

Introduction

Most of us with older parents probably have

some sense of how much sixpence really used to buy (and how little it buys now).

This article examines a recently announced 6p per kWh EV charging tariff in the

UK.

A bit

about Ovo Energy

Ovo Energy was established in Bristol,

England in 2008 as domestic electricity and gas trader, and grew steadily by

acquisition. In early 2020 Ovo

acquired Scottish & Southern Energy’s 3,500,000 home energy customers, making

Ovo one of the largest electricity suppliers in Britain.

Ovo’s 6p

tariff

In late January 2021, Ovo announced a new

EV tariff of a flat rate of 6p per kWh anytime, which Ovo hopes will rival its

competitors low off-peak EV charging tariffs. Taken at face value, that

suggests it would cost about £1.50 to buy 110km worth of electricity for an early

model Nissan Leaf.

Ovo’s modelling of EV driver behavior

suggests that there will be enough idle EV’s willing to V2G (vehicle to grid)

to offset those wanting anytime charging. A quick comparison of EV tariffs

reveals…

|

Supplier |

Off-peak tariff |

Any-time tariff |

|

Ovo |

6p |

|

|

EDF Energy |

4.5p |

14.3p |

|

British Gas |

|

19.5p |

|

E.On |

10.4p |

|

The

type-of-use tariff

Ovo has framed this tariff as a “type of

use” tariff, which seems quite novel. A little thought, however, reveals that

type-of-use tariffs have been around forever eg. hard-wired

space heating that only worked when a separate circuit was energized. While it

could be argued that this was in fact a time-of-use tariff (because it went on

and night and off during the day), it was primarily a type-of-use tariff because

of its unique purpose.

Energy mix and grid security

US – designating must-run

generation

Introduction

Pipes

& Wires #192 noted that the California Independent System Operator (CaISO)

had sought approval from the Federal Energy Regulatory Commission (FERC)

for broader authority to use Reliability Must Run (RMR) designations. This

article notes a recent RMR designation specifically to reduce the risk of

blackouts during the 2021 summer.

The RMR

designation

In December 2020 the CaISO

designated the 250 MW Midway

Sunset Cogeneration plant as RMR,

meaning that Midway has to keep the plants available on prices, terms and

conditions acceptable to the CaISO.

The background to the RMR designation was

that in September 2020 Midway sought approval from the CaISO to retire 2 units

on 31st December 2020 following the retirement of a third unit earlier

in 2020. This would’ve left insufficient contingent capacity for the CaISO to

meet various real-time grid security obligations, hence the RMR designation.

Further

reading

Readers might be interested in the

following articles which explore must-run requirements and proposed payment

methods.

· Pipes

& Wires #177 examined the

various views around designating gas-fired generation in California as RMR.

· Pipes

& Wires #138 examined the

German regulators’ requirement to seek approval to close generation capacity.

· Pipes

& Wires #119 examined who

should pay for standby generation in Germany.

Ukraine – 35 years on from Chernobyl

Introduction

Next

month (April) will be the 35th anniversary of the explosion at the V I Lenin Chernobyl Power Station ... an event that many in Eastern

Europe are still painfully reminded of. This article examines Chernobyl in

detail and tries to uncover a bit more of what really happened there.

Some facts about Chernobyl power

station

The

station itself is 18km north-east of the city of Chernobyl, and at the time of

the explosion in 1986 was supplying about 10% of the Ukraine’s electricity

through the 330kV and 750kV grids. Construction began in 1970 and the first 4 RBMK-1000

reactors (rated at 3,200 MWt) were commissioned in 1977, 1978, 1981

and 1983 respectively. Reactors #5 and #6 that were under construction at the

time of the explosion were rapidly abandoned.

Essentially

the RBMK reactor is a graphite moderated, boiling water reactor (BWR) that was derived from a

plutonium-producing military reactor. A critical feature of the RBMK is that

when the cooling water boils to steam, its neutron absorbing capacity drops to near

zero. This means more neutrons are available to fission the 235U

nuclei, increasing the heat generation and in turn flashing more water to steam

and further reducing the neutron absorption (giving the RBMK a very high

positive void coefficient). A high positive void coefficient

didn’t necessarily make the RBMK inherently unsafe as this runaway can take

several seconds or even minutes, theoretically giving time to bring the

reaction back under control.

Reactors

#3 and #4 were second generation RBMK’s that had a number of improved safety

features which reactors #1 and #2 did not have.

What actually happened on 26th

April 1986 ?

The explosion

arose from an experiment to test whether the run-down of the turbine following

a trip could provide sufficient electricity for the cooling water pumps while

the auxiliary diesel generators were started and synchronised. Desk-top studies

suggested it would work however 3 attempts to achieve this in practice over the

3 previous years had all failed.

At

1:23am on 26th April 1986 a 4th attempt at the experiment

began by tripping the steam from reactor #4, which was followed by a run-down of

the turbine and 4 of the 8 cooling water pumps. In the 39 seconds before the

diesel generators were synchronised the cooling water flow dropped sufficiently

to allow voids in the cooling water circuit to form. Although this started a

positive feedback cycle, automatic control of the graphite control rods

successfully reduced that increased heat generation. At 1:23:40am an emergency

shutdown was initiated (and whether this was manual or automatic remains

debated to this day). Unfortunately the design of the reactor resulted in

cooling water being expelled a few seconds before the graphite rods filled the

voids, resulting in a thermal runaway which was followed a few seconds later by

an explosion accompanied by the last recorded power output of about 33,000 MWt

(10x nominal rating). A 2nd explosion followed, the precise cause of

which remains undetermined.

Note

that this was the 2nd of 3 incidents that occurred, the first being

a partial core meltdown on reactor #1 in 1981, and the third being a simple

non-nuclear generator hydrogen leak on turbine #4 (associated with reactor #2).

What happened after the 26th

April 1986 ?

Seconds

after the second explosion, the 2,000 ton upper plate of the reactor vessel was

torn lose and blown off, and flaming material caused at least 5 separate fires

on the bitumen-coated roof. Some 3 hours later at about 5:00am the reactor was

shut down at the instruction of the night shift superintendent.

Evacuation

of the nearby town of Pripyat began at 2pm on 27th April, almost 37 hours

after the explosion, however there was still no official word of the explosion

until 3 days later on 29th April when radiation alarms at Forsmark power station in Sweden were activated. To this day

a 30km exclusion zone still exists around Chernobyl.

Network regulatory decisions

Aus – the

Powerlink revenue determination

Introduction

Powerlink recently submitted its Regulatory

Proposal (rate

case) to the Australian Energy Regulator (AER) for the 5 year control period

commencing on 1st July 2022. This article sets some context for

examining the AER’s draft and final decisions.

A bit about Powerlink

Powerlink owns and operates the

high voltage transmission grid that stretches from the Gold Coast in the south

to Cairns in the north, comprising 15,300km of lines and 140 grid substations.

Powerlink is owned by the Queensland State Government, and has an annual

revenue of about $700m.

Regulatory framework

The

basis of the regulatory framework is Chapter 6a of the National Electricity Rules, which is made pursuant to the National Electricity Law.

Key features of the process to date

Key features of the Powerlink

process to date include…

|

Parameter |

Proposal |

Draft Determination |

Revised Proposal |

Final Determination |

|

CapEx |

$864m |

|

|

|

|

OpEx |

$1,029m |

|

|

|

|

Opening RAB |

$6,958m |

|

|

|

|

Post-tax nominal WACC |

4.44% |

|

|

|

|

Depreciation |

$881m |

|

|

|

|

Smoothed revenue |

$3,565m |

|

|

|

Pipes & wires will comment

further once the AER releases its draft decision.

Industry reshuffling

India –

consolidating distribution businesses

Introduction

Most of us are familiar with consolidation

of distribution businesses … Pipes & Wires recent examination of Western

Power Distribution in the UK is a good example. This article examines the

planned consolidation of the non-Kolkata distribution subsidiaries of the RP-Sanjiv Goenka

(RPSG) Group in India.

A bit

about RP-Sanjiv Goenka

The RPSG Group is an industrial services

group based in Kolkata with annual revenues of about US$4b. Its electric

distribution businesses include the Calcutta Electric

Supply Corporation (CESC), which in

turn has 5 subsidiaries that hold distribution licenses outside of Kolkata…

· Noida Power Company Ltd (joint

venture between RPSG and the Greater Noida Industrial Development

Authority).

· Kota Electricity

Distribution.

· Bikaner

Electricity Supply Ltd.

· Bharatpur

Electricity Services Ltd.

In additional to these 5 distribution

subsidiaries, there are also several coal mining and coal-fired generation subsidiaries.

The

planned consolidation

It is proposed to consolidate the 5

subsidiaries into 1 business called Eminent Electricity Distribution to improve

focus and strip out costs. Eminent will be a wholly-owned subsidiary of CESC

with an annual revenue of about US$485m.

This consolidation represents a significant

reversal of RPSG’s originally proposed strategy of inter alia demerging the distribution and generation businesses.

Section 17(3) of the Electricity Act

2003 requires

regulatory approval to either assign a license or transfer any part of a

business, which the West

Bengal Electricity Regulatory Commission

declined to do.

South

Africa – progress on splitting off Eskom transmission

Introduction

Previous issues of Pipes & Wires have

examined Eskom’s

proposal to split off the transmission business to inter alia provide third-party generators with confidence that grid

access will be transparent with respect to Eskom’s own generation. This article

examines recent progress.

Recent

progress

Eskom has recently announced that it plans

to complete the legal separation of its transmission business by the end of

2021, followed by legal separation of generation and distribution during 2022.

A key issue will be the allocation of Eskom’s debt amongst the separated

businesses.

Further

reading

Further reading includes…

· Pipes

& Wires #194 – introduction,

and a range of views.

· Pipes

& Wires #202 – presentation of

generic models for splitting off transmission.

Pipes & Wires will revisit this story

later in 2021.

General stuff

Guide to NZ electricity laws

I’ve

compiled a “wall chart” setting out the relationship between various past and

present electricity Acts, Regulations, Codes etc in

sort of a chronological progression. To request your free copy, pick here. It looks really cool printed in color

as an A2 or A1 size.

A bit of light-hearted humor

What

if price control had been around in the 1920’s and 1930’s ?

A collection of classic historical photo’s with humorous captions looks at some

of the salient features of price control. Pick here to download.

A potted history of electricity

transmission

I’ve

recently compiled a potted history of electricity transmission. Pick here to download.

Wanted – old electricity history books

Now

that I seem to have scrounged pretty much every book on the history of

electricity in New Zealand, I’m keen to obtain historical book, journals and

pamphlets from other countries. So if anyone has any unwanted documents, please

email me.

Opt out from Pipes & Wires

Pick

this link to opt out from Pipes & Wires.

Please ensure that you send from the email address we send Pipes & Wires

to.

Disclaimer

These articles are of a general nature, they do not constitute specific

legal, consulting or investment advice, and are correct at the time of writing.

In particular Pipes & Wires may make forward looking or speculative

statements, projections or estimates of such matters as industry structural

changes, merger outcomes or regulatory determinations. These articles also summarise lengthy documents, and it is important that readers refer to those

documents in forming opinions or taking action.

Utility Consultants Ltd accepts no liability for action or inaction

based on the contents of Pipes & Wires including any loss, damage or

exposure to offensive material from linking to any websites contained herein,

or from any republishing by a third-party whether authorised or not,

nor from any comments posted on Linked In, Face Book or similar by other

parties.

{kind=link}