From the editor’s

desk…

Welcome

to Pipes & Wires #101. This month continue the recent theme of mergers in

the US electric industry, and then also look at 2 topical security of supply

issues in the US.

We

also examine a wide range of energy and regulatory policy decisions from around

the world, and conclude with a look at a gas transmission regulatory decision

in Australia.

Accredited supplier status

Utility

Consultants is pleased to announce that it is now an Asia-Pacific Utilities Group (APUG) accredited

supplier (registration number 88899493).

Get Pipes & Wires “white-listed”

To

avoid being intercepted by your server as spam, please arrange to have phil.caffyn@utilityconsultants.co.nz

“white-listed” by your IT people.

Pipes & Wires on the web

Pipes & Wires on Linked In

Pipes

& Wires now has an on-line

group for readers to keep in touch on a more regular basis, bounce ideas

around or raise issues and concerns. Pick here

to visit my Linked In profile and add me

to your connections.

Pipes & Wires on Facebook

Pipes

& Wires now also has its own Facebook

page. Just go to Facebook’s home page and search for Pipes & Wires.

Pipes & Wires on YouTube

To

see a short video clip explaining more about Pipes & Wires, pick here.

Pipes & Wires on the web

To

read more about Pipes & Wires, pick here.

About Utility Consultants

Utility

Consultants Ltd is a management consultancy specialising in pretty much all aspects of energy and infrastructure

networks – pick here

to see more, or to be sent a detailed profile of recent projects, pick

here.

Mergers & acquisitions

US – AES makes a bid for Dayton Power

& Light

Introduction

The

US electric power industry has seen a flurry of recent mergers, and indeed Pipes

& Wires #100 indicated that it would be surprising if further mergers

didn’t emerge in the near future. This article examines AES Corporation’s recent cash bid for

DPL Inc.

A bit about the key players

The

key players of this deal are:

·

AES Corporation is a multi-national

utility, with 132 generation plants in 28 countries, and US$17b in annual

revenues.

·

DPL supplies 500,000 electric customers

in western and central Ohio, and has annual revenues of US$1.9b.

The proposed deal and its’ drivers

This

deal is fairly simple ... AES will pay $30 cash for each share of DPL’s common

stock, which represents about an 8.7% premium to DPL’s closing price. Key

drivers of the deal include:

·

The need for AES to reduce its high

exposure to declining wholesale electricity prices by forward integrating into

a retail customer base. However this may only buy about 18 months of high

prices as DPL’s current regulated retail price (which is about 25% higher than

market prices) expires in late 2012.

·

The need for AES to improve the returns

on its cash reserves.

·

DPL’s strength of future earnings due

to pre-existing emission controls on its coal-fired plants.

·

Possible synergies between DPL and AES

subsidiary Indianapolis

Power & Light.

So it would appear that the drivers for

this deal are somewhat different from other recent deals which have been driven

by the need to increase scale to better fund emission controls and new

transmission investment. It is also likely that a much narrower array of

regulatory approvals will be required as DPL only operates within 1 state.

US

– Exelon makes a bid for Constellation

Introduction

Following

on from the comments in the previous article that it would be surprising if

further mergers didn’t emerge in the near future, this article examines Exelon Corp’s recent bid for Constellation Energy Group.

The

key players

The key players in this deal are:

·

Exelon

owns 32,000MW of generation and supplies 5,400,000 electric customers in

northern Illinois and southern Pennsylvania. Annual revenue is about $19b.

·

Constellation

owns 12,000MW of generation and supplies 1,200,000 electric and 630,000 gas

customers in Maryland (through its subsidiary Baltimore Gas & Electric).

Annual revenue is about $14b.

Some

details of the bid

Exelon is offering 0.93 of its shares for

each Constellation share, valuing the deal at about $7.7b and representing a

premium of about 12.5% over Constellation’s closing price.

Key

drivers of the bid

Likely drivers of the deal include geographical

synergies between Exelon’s service territory in southern Pennsylvania and

Constellation’s BGE territory in Maryland, and possibly some forward

integration into BGE’s retail market to ease the effect of soft wholesale power

markets.

US - a running total of recent deals

Just

so we can keep track of it all, recent and present deals in the US include:

|

Deal |

Consideration |

Premium |

Dimensions of

merged entity |

|

PPL’s acquisition of LG&E and KU (from E.On US) |

$5.6b

cash and $800m debt |

|

20,000MW

of generation, 2,600,000 electric customers |

|

First Energy Corp

acquires Allegheny

Energy |

$4.4b

in stock and $3.8b debt |

10.8% |

23,700MW

of generation, 6,000,000 electric customers, annual revenue of $16b. |

|

Northeast Utilities acquisition of NStar |

$4.17b

in stock |

0% |

3,000,000

electric and 505,000 gas customers, annual revenue of $8.4b. |

|

Duke Energy’s acquisition

of Progress Energy |

$13.8b

in stock and $12.2b debt |

4% |

56,000MW

of generation, 7,100,000 electric customers. |

|

|

$3.5b

cash |

8.7% |

Annual

revenue of $19b, 970,000 electric customers. |

|

Exelon’s bid for Constellation |

$7.7b

in stock |

12.5% |

44,000MW

of generation, 6,600,000 electric customers, annual revenue of $33b. |

Asset strategy

US – using batteries to complement wind

Introduction

Most

of us are very aware of the limitations of wind. This article examines Duke Energy’s use of batteries at a

Texas wind farm to provide power when the wind stops blowing.

The specific technology

The Notrees wind farm will have 36MW of battery banks, provided by Xtreme Power of Austin, Texas. The specific technology is Xtreme’s

PowerCells which are essentially 12V, 1kWh

ultra-low impedance dry-cell batteries and a whole bunch of fancy electronics

(collectively called the Dynamic Power Resources).

What about the $$$

So

what’s it all costing ? The Notrees DPR

will cost $43m (which includes a Department of

Energy grant of $22m), so on the face of it that looks like about

$1,200/kW. A bit of rough (and indeed simplistic) analysis would suggest that

this is towards the low end of installed costs, and that batteries could well

be a good alternative to, say, gas turbines for complementing an existing wind

farm.

Industry reshuffling

Aus – reshuffling the Queensland

generators

Introduction

Breaking

up monolithic generators as part of the industry reform process is certainly

nothing new, however the relative competitiveness of the resulting generators

can often be a vexing issue. This article examines the recent restructuring of

generation businesses in the Australian state of Queensland.

The original breakup

The

original breakup of the former Queensland Electricity Commission (which

transitioned through Austa Electric) resulted in the following generation

companies:

·

CS Energy – Callide,

Swanbank, Mica Creek (not NEM connected) and Kogan Creek (constructed after break up).

·

Tarong Energy – Tarong, Wivenhoe and Tarong North (constructed after breakup).

·

Stanwell Corporation – Stanwell,

Mackay and several smaller hydro’s.

The Gladstone

power station asset (but not the power purchase agreement) was sold to Comalco in March 1994 prior to the reform process.

The current issue

Around

the time when the 3 competing generators were established, each Australian

state operated its own electricity market, and moreover most electricity was

sold on-market. Each of the 3 generators had a similar (or at least not wildly

dissimilar) cost advantage.

Pipes

& Wires #51 examined the sale of Energex and Ergon Energy’s retail businesses ahead of full retail contestability

(FRC). The resulting sales of Energex’

retail business to Origin Energy

and Ergon’s large customer retail business to Australian Gas Light (AGL) in 2007 and the

subsequent vertical integration has depressed wholesale prices. While this

might be good news for customers, it makes it difficult for legacy coal-fired

plant to compete.

The new structure

The

proposed restructuring will see a consolidation of the 3 existing generators

into 2 larger generators as follows:

·

CS Energy – Callide B, Callide C, Kogan Creek, Wivenhoe and

the Gladstone power purchase agreement

·

Stanwell Tarong – Stanwell, Tarong, Tarong North, the Collinsville power purchase agreement, Swanbank

E, Mica Creek (not NEM connected), the hydro’s, and the retirement of Swanbank

B.

The

new companies take effect from 1st July 2011, and it will be

interesting to see whether the reshuffling and consolidation has improved the

cost position.

Austria – unbundling gas transmission

Introduction

Unbundling

of lines and energy as part of the energy sector reform process is certainly

widely understood, even if still largely controversial. This article briefly

examines the proposed unbundling of Austria’s gas transmission system operators

(TSO’s) under laws pursuant to the EU’s Third Package.

The EU Third Package

The EU’s

Third Energy Package of September 2007 aimed to benefit all citizens by

providing greater choices and fairer prices. Highest amongst the EU’s proposed

approach was unbundling of lines and energy, with the consequent requirement

for all member countries to implement unbundling. The EU’s initial thoughts

proposed 2 options for unbundling, viz:

· Full ownership separation of lines (probably including

pipes) and energy.

· Retaining ownership but placing full operational and

investment control in the hands of an independent system operator (ISO).

Early

July 2008 saw the EU Parliament

reject forced unbundling of vertically integrated gas businesses, siding with

many member countries. That diluted draft law would require internal separation

… the much applauded “Third Way” … which represents a significant watering down

of the ISO option. In regard to electricity, however, it seemed the EU is

determined to have nothing less than full ownership unbundling. The Package was

finally passed into EU law in September 2009, with individual member countries

having 18 months to implement those reforms via their own legislation.

The utilities to be unbundled

The

TSO’s that will have to unbundle are:

·

OMV

Gas GmbH, which owns and operates 2,000km of transmission pipelines within

Austria and represents a major European hub.

·

TAG GmbH, which operates a 380km

gas transmission pipeline between Baumgarten and Arnoldstein.

·

BOG

GmbH, which holds the marketing rights for the 245km gas transmission

pipeline from Baumgarten to Oberkappel.

The proposed unbundling

It

appears that each of the TSO’s will have to choose between Ownership

Unbundling, ISO and the “Third Way” (management and investment being controlled

by a separate subsidiary). There are understandably a range of industry

reshuffling, market positioning and commercial issues around each option, so

this will be worth watching.

Energy policy

US – what future hath coal ?

Introduction

Pipes

& Wires #90 included an article with this somewhat witty heading, and

it seemed appropriate to recycle it for this article which examines Senate Bill 5769

in the US state of Washington which aims to close the almost 40 year old 1,460MW

Centralia coal-fired power station by 2025. To give it some perspective, Centralia

generates between 8% and 10% of Washington’s electricity.

A few details of Senate Bill 5769

Senate Bill 5769 recites at length the

state’s concern about the toxic residues of coal combustion, and how previous

commitments to reducing CO2 emissions require further action. In

particular, any electric generating station that emitted more than 1,000,000

tons of greenhouse gases in each of the calendar years 2005, 2006 and 2007 will

be subject to an emissions standard applicable from 31st December

2020. A “qualifying facility” may petition the Governor to defer the

applicability of the standard until 31st December 2025 at the

latest.

Around the time of writing this article,

the Senate had voted 33-14 to send the Bill to Governor Christine Gregoire, who then

signed the Bill into law.

What the stakeholders are saying

So what are all the stakeholders saying

? A search of the local news reveals an unsurprising diversity of opinions:

·

Centralia’s owners, TransAlta, seem broadly accepting of the Bill, presumably recognising that phasing out coal is the way of the world at the

moment. TransAlta does however note that the amendments don’t significantly

alter a previously reached joint agreement between TransAlta, the state government, organised labor and environmental groups (Editor’s note – it might be

questioned why any variation from a prior agreement occurred at all).

·

Environmental groups seem delighted,

with the closure not coming soon enough for some.

·

Centralia employees are unhappy that

job losses are almost certain to occur (and with no other coal-fired plants in

Washington, that would mean relocating inter-state for many).

·

Officials from the Centralia area are

unhappy that the plant closure would be another economic loss to the community

(about $26m in wage per year).

·

Consumer lobbyists are unhappy with the

likely price of replacement generation.

·

Representatives (judging by the

overwhelming 87 to 9 support for the Bill) seem happy with the Bill.

Has anyone considered security of supply ?

On the whole, it would appear not. It

is certainly not clear that the gas-fired combined cycle plant that TransAlta will be incentivised to

replace Centralia with will replace all 1,460MW. So the funny thing is that

Washington may end up importing coal-fired electricity from other states (which

it already does in the form of a coal-fired station in Montana owned by Puget

Sound Energy). Gee ... where have we come across that before ? Like ... uh ...

anti-nuclear Germany importing nuclear electricity from France and the Czech

Republic !!!

France – downward pressure on feed-in tariffs

Introduction

The area of feed-in tariffs has had a

rather rapid path to maturity, with several jurisdictions rapidly reducing the

tariff as it became apparent that many people’s motivation was simply financial

rather than environmental. This article examines the new regulatory framework

for photo-voltaic (PV) generators in France, and then examines some wider

general policy issues.

A bit of background to the French PV sector

Installed PV capacity has grown rapidly

in France, from 81MW at the end of 2008 to 1,025MW at the end of 2010, which is

pretty close to France’s target of 1,100MW by the end of 2012. Like several

jurisdictions, France curtailed the former feed-in tariffs to reduce

“inflation” in the PV sector, even going as far to use the phrase “excessive

returns”. This created a period of uncertainty until the recently announced

regulations commenced.

The French regulatory framework

Key elements of the French PV

regulatory framework include:

·

PV plants up to 100kW will be paid a

feed-in tariff that will initially be 20% lower than the tariffs that were in

force on 1st September 2010, and will be reviewed quarterly.

·

Larger plants will submit tenders

(presumably like the German and Californian “reverse auction” model).

·

The government expects future tariff

reviews to reflect an expected cost reduction of 10% per year.

·

A requirement to dismantle and recycle

PV plants at the end of their lives.

Media commentary suggests that the

French tariff reductions may well encourage similar reductions in Germany and

the Czech Republic.

Some wider issues on the whole renewables sector

Probably the most significant issue is

how this whole feed-in tariff thing has become such a double-edged sword to the

policy makers and regulators, so just a couple of observations to close this

article:

·

On one hand renewables (especially PV) are

the darling of many bureaucrats, but on the other hand the high uptake has

ostensibly been for the filthy lucre rather than to save the planet.

·

A whole industry has been built around

renewables and subsidies, and that industry (along with the Green parties) is

understandably upset that those subsidies (the feed-in tariffs) are being

reined in.

·

Those advocating subsidies for

renewables are finding themselves caught in the gulf between “the fossil fuel

industry got plenty of subsidies” on the one hand and on the other hand subsidies

being unacceptable in these apparently more enlightened times.

·

The true costs of the renewable

industry and the jobs it has created are becoming more visible (I read

somewhere a while back that each renewable energy job created in somewhere like

Spain or Portugal was costing 3x the average wage).

Regulatory policy

Belgium – protecting consumers from

price volatility

Introduction

One

of the key purposes of energy sector reforms is to firstly put downward

pressure on prices, and secondly to ensure that any resulting price reductions

are shared with customers. This article examines whether there might be a

disconnect in Belgium’s proposed legislation between wanting to pass on price

reductions to customers on the one hand, but protect customers from price

volatility on the other hand.

Background

The EU’s

Third Energy Package that was released in September 2007 set out several

ambitious goals for Europe’s energy sector that included options for unbundling

lines from energy, improving security of supply particularly during gas supply

interruptions, and improved customer rights. Earlier in 2011, the Commission

de Régulation de l'Électricité et du Gaz (CREG) published a

position paper on implementing the Third

Package that discussed

inter alia how customers might be

protected from price volatility.

Thinking about price volatility

Perhaps

a good starting point to examine this issue would be the strong coupling of

Belgium’s gas and electricity prices to the price of underlying gas imports

from Russia and the Middle East. Implicit in that underlying gas price will be

a level of volatility that is only likely to increase, so one way or another

the electric and gas utilities in Belgium will be exposed to price

volatilities.

Those

utilities could take (broadly) either of 2 approaches:

·

They could pass on that volatility (and

the associated volatility risk) to their customers, who would accept the price

swings.

·

They could absorb that volatility (and

risk) and expose their customers to more certain prices. In doing so, they

would need to charge a premium for accepting that risk.

It would appear, however, that the officials’

preference would be for the utilities to pass on the low prices whilst

absorbing high prices, a kind of customers having it both ways sort of approach.

So it will be interesting to see how the utilities respond to any final legal

requirements along those lines.

UK – setting the framework for RIIO-GD1

Introduction

The UK’s gas distribution companies are currently

subject to GDPCR

2007-13, which runs from 1st April 2007 until 31st

March 2013. As most of us will be aware, this GDPCR is based on the RPI-X

approach. This article examines OFGEM’s RIIO-GD1

which will reflect the new Revenue = Incentives + Innovations + Outputs

approach resulting from the recent RPI-X @ 20 review.

A quick recap of the RPI-X @ 20 review

Back in 2008, OFGEM announced that the RPI-X approach

would be substantially overhauled. A few

of the issues that need to be considered going forward include….

·

The formation of a new EU-wide

regulatory body.

·

The EU’s views on vertical integration

of the energy giants.

·

Climate change and renewable

obligations.

·

Increasing complexity of price

controls.

·

The end of “easy” OpEx efficiency

gains.

·

Concerns that the RPI regime is moving

toward a Rates-based regime.

·

Concerns that valuation and financial

parameters and principles may have become less valid over time.

·

The need to properly recognise

increased security requirements since 9/11 and 7/7.

In

late July 2010, OFGEM released a consultation

paper setting out its proposed adoption of the RIIO Model – “revenue set to

deliver strong incentives, innovation and outputs”. Some of the significant

headline features include...

·

An “outputs led” philosophy in which

the price control would focus on lines businesses delivering specified

outcomes.

·

Retention of ex-ante control which

would include a return on RAV.

·

A commitment to publishing the

principles for setting a WACC-based return, with subsequent cross-checking

against credit ratings.

OFGEM

was also of a mind to establish an 8 year control period with a mid-term

review, and also anticipated the EU’s “Third Package”

of energy reforms which any emerging regulatory framework must be consistent

with.

Key elements of RIIO-GD1

The key elements of RIIO-GD1

are broadly as follows:

· Increased flexibility to deliver

what customers want from a network (as distinct from delivering a

pre-determined set of price, capacity, security and reliability outcomes).

· Lengthening the price control

from 5 to 8 years to encourage a longer-term focus.

· Higher returns for delivering

high quality services at lower costs, with the incentive of avoiding more

intrusive price controls.

· Allowing new entrants to take

responsibility for large investment projects.

· Providing clear investment

signals to investors to ensure utilities remain financeable.

· An expectation that distribution

companies will engage more routinely and regularly with their customers to

better determine those customers’ preferences.

This all sounds very grand, and indeed those who have

examined the EU’s expectations of “Increased Choice – Lower Prices – Improved

Security” might notice some common themes. In particular it will be interesting

to see exactly how (and the priority that is given to) those investment signals

end up. Pipes & Wires will follow this one closely as news emerges.

Regulatory decisions

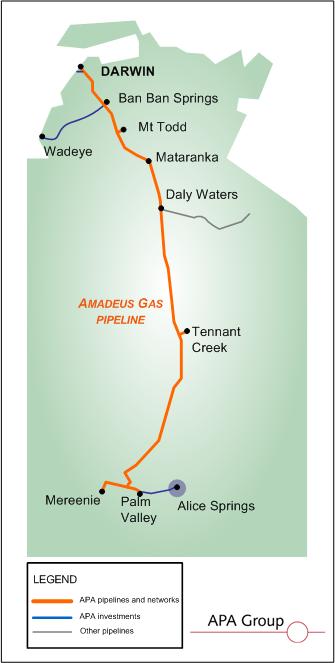

Aus

– the Amadeus Gas Pipeline draft decision

Introduction

Pipes & Wires has worked its way around

the access arrangement decisions for most of Australia’s gas transmission

pipelines. This article examines the Australian

Energy Regulator’s (AER) recent draft

decision to not accept NT Gas’ proposed access arrangement for the Amadeus Gas Pipeline (AGP)

for the period 1st July 2011 to 30th June 2016.

A

bit about the Amadeus Gas Pipeline

The AGP stretches 1,658km from Palm Valley

and Mereenie in central Australia to Darwin, and has a capacity of about 100TJ

per day. The sole connected user of the AGP is the Power & Water Corporation,

for the supply of its gas-fired generation.

The

legal framework

The AER’s powers and duties, including with

respect to regulating the AGP, are set out in the National

Gas Law (NGL) and the National

Gas Rules (NGR). The NGL requires the AER to perform its functions in a

manner likely to contribute to the National Gas Objective “to promote

investment in, and efficient operation of, natural gas services for the long

term interests of consumers of natural gas with respect to price, quality,

safety, reliability and security of supply of natural gas”.

The

draft decision

The following table compares the AER’s

draft decision with NT Gas’ proposed access arrangement (and will be completed

as the revised arrangement and final decision come to hand):

|

Component |

Proposed access arrangement |

Draft decision |

Revised access arrangement |

Final decision |

|

Total revenue requirement |

$169.8m |

$129.7m |

|

|

|

Reference tariff |

$0.7596/GJ/day |

$0.5778/GJ/day |

|

|

|

Nominal risk free

rate |

5.48% |

5.53% |

|

|

|

Inflation forecast |

2.50%/yr |

2.57%/yr |

|

|

|

Real risk free

rate |

2.66% |

2.89% |

|

|

|

Cost of debt |

10.94% |

9.32% |

|

|

|

Debt risk premium |

5.46% |

3.79% |

|

|

|

Cost of equity |

11.98% |

10.335% |

|

|

|

Equity beta |

1.00 |

0.80 |

|

|

|

Market risk

premium |

6.50% |

6.00% |

|

|

|

Gearing |

60% |

60% |

|

|

|

Nominal vanilla WACC |

11.36% |

9.72% |

|

|

|

Opening capital base |

$112.4m |

$97.0m |

|

|

|

CapEx |

$14.4m |

$13.9m |

|

|

|

OpEx |

$73.0m |

$58.6m |

|

|

The AER’s draft decision is to not accept

the proposed access arrangement, and to require NT Gas to make a number of

specific revisions. Pipes & Wires will make further comment as the revised

arrangement and the final decision emerge.

A bit of light reading…

Wanted – old electricity history books

If

anyone has an old copy of the following books (or any similar books) they no

longer want I’d be happy to give them a good home…

·

White Diamonds North.

·

Northwards March The Pylons.

·

Marlborough Will Shine Through.

·

Two Per Mile.

·

Live Lines (the old ESAA journal)

Conferences & training courses

The following

training courses will be run by Conferenz...

·

ENEX

– New Zealand’s Oil & Gas Event – New Plymouth, 9th – 10th

June, 2011.

Opt out from Pipes & Wires

Pick

this link

to opt out from Pipes & Wires. Please ensure that you send from the email

address we send Pipes & Wires to.

Disclaimer

These articles

are of a general nature and are not intended as specific legal, consulting or

investment advice, and are correct at the time of writing. In particular Pipes

& Wires may make forward looking or speculative statements, projections or

estimates of such matters as industry structural changes, merger outcomes or

regulatory determinations.

Utility

Consultants Ltd accepts no liability for action or inaction based on the

contents of Pipes & Wires including any loss, damage or exposure to

offensive material from linking to any websites contained herein.

{kind=link}